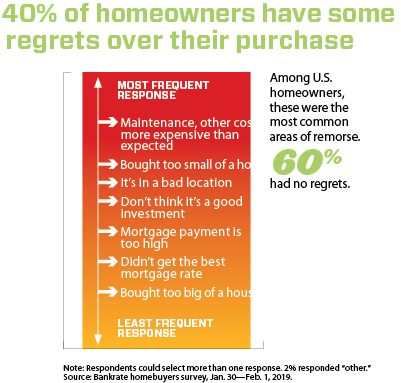

As affordability pressures continue to shape buyer behavior nationwide, Google searches for “help with mortgage” have reached their highest level since 2009, even as 30-year rates ease into the low-6 percent range. The disconnect is clear: rates alone are no longer the primary barrier. Payments, inventory and overall cost of ownership are.

While agents increasingly rely on tools like temporary buydowns, seller credits and assumable loans to help buyers bridge affordability gaps, one solution remains consistently overlooked: manufactured housing.

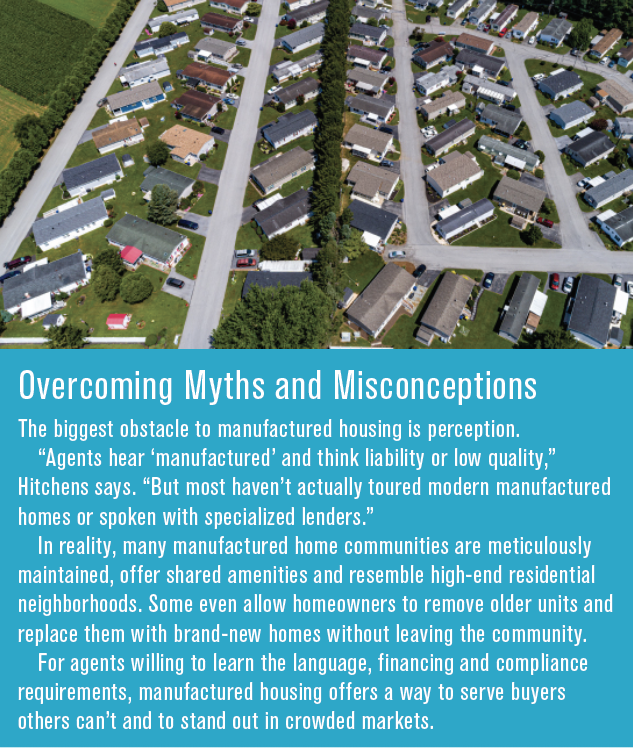

For many real estate professionals, manufactured homes remain a blind spot, avoided due to outdated perceptions, lack of education or uncertainty around financing and regulations. Yet for buyers priced out of traditional site-built homes, manufactured housing can offer a viable, high-quality and often wealth-building path to ownership. For agents willing to specialize, it also represents a powerful niche opportunity.

Why Manufactured Housing Belongs in the Affordability Conversation

Why Manufactured Housing Belongs in the Affordability Conversation

“Manufactured homes are one of the most underutilized solutions we have right now,” says Yvette Hitchens, CRS, broker-owner of Pacific Estates in Long Beach, California, and founder of The MH Trainer. “Affordability is driving everything, and manufactured housing directly addresses that challenge.”

A manufactured home is defined as a home built after June 15, 1976, in compliance with U.S. Department of Housing and Urban Development construction standards. These standards govern everything from electrical systems and wind resistance to energy efficiency and safety. Homes built before that date are classified as mobile homes and do not meet the same criteria, an important distinction many agents and consumers misunderstand.

Unlike stick-built homes, manufactured homes are constructed in controlled environments, reducing material waste, weather delays and inconsistencies. Once completed, they are transported to their site and installed on either owned land or leased land within a manufactured home community.

“The quality is there,” Hitchens says. “People still picture trailers, but today’s manufactured homes are well-designed, durable and often indistinguishable from site-built homes once installed.”

Financing Realities

One reason agents shy away from manufactured housing is complexity, particularly around financing. Understanding the difference between on-land and land-leased manufactured homes is essential.

Manufactured homes placed on owned land can qualify for VA, FHA and conventional financing, much like site-built properties. In these cases, the home is titled as real property.

Homes located in land-lease communities, where the buyer owns the home but leases the land, are typically financed through chattel loans, which treat the home as personal property. These loans require specialized lenders and differ significantly from traditional mortgages.

“This is where deals often fall apart,” Hitchens explains. “Agents write offers with pre-approvals from traditional lenders who don’t finance manufactured homes. Education is everything.”

Despite the added complexity, the math often works strongly in the buyer’s favor. A buyer paying $1,000–$1,200 on a chattel loan plus an $800–$1,000 land lease may still come in well below local rents or traditional mortgage payments.

In some high-cost California markets, Hitchens has seen manufactured homes purchased decades ago for under $50,000 sell for well over $500,000, challenging the myth that manufactured homes automatically depreciate.

Manufactured Homes as a Strategic Niche for Agents

For agents, manufactured housing is not just an affordability solution but rather a business opportunity.

“There’s almost no formal education for agents in this space,” Hitchens says. “That creates fear, but it also creates opportunity for the agents who step in and learn it.”

Hitchens holds dual licensure through the California Department of Real Estate and the Department of Housing and Community Development (HCD), which oversees manufactured housing. In California, agents can handle resales of manufactured homes, but selling brand-new homes from the factory requires additional licensing or working under a dealer.

Rather than seeing this as a barrier, Hitchens saw a gap and built a specialization around it.

“When you become known as the agent who understands manufactured housing, the referrals follow,” she says. “First-time buyers, downsizers, veterans and workforce households are actively looking for guidance.”

Manufactured housing appeals most strongly to two groups: first-time buyers and downsizers.

First-time buyers benefit from lower purchase prices, smaller payments and faster paths to ownership. Downsizers, particularly in 55-plus communities, often use proceeds from a traditional home sale to purchase a manufactured home outright, reducing monthly expenses while preserving savings.

Veterans represent another important segment. In some states, VA and state-specific programs allow financing of manufactured homes placed on owned land. Hitchens notes growing regulatory interest in expanding financing options further, particularly as affordability pressures intensify nationwide.

Reframing the Affordability Conversation

Manufactured homes also pair naturally with other affordability tools agents are already using, such as temporary interest-rate buydowns.

Temporary rate reductions, like 2-1 buydowns, can help buyers manage payments during the early years of ownership while maintaining long-term equity. When combined with a lower purchase price, such as a manufactured home, these tools can dramatically improve affordability outcomes.

In practice, this allows agents to build custom financing stacks: pairing home type, loan structure, seller credits and buydowns to meet buyers where they are.

The key, as always, is education. Buyers don’t need mortgage theory; they need clarity around payments, ownership and long-term options.

A Call to Expand the Toolbox

A Call to Expand the Toolbox

As affordability challenges persist, real estate professionals can no longer rely on one-size-fits-all solutions. Manufactured housing deserves a place alongside buydowns, seller credits and other creative financing strategies in a modern agent’s toolkit.

“The buyers are there,” Hitchens says. “They just need someone confident enough to show them what’s possible.”

For CRS designees and residential specialists, understanding manufactured housing isn’t about leaving traditional real estate behind; it’s about expanding expertise, serving underserved clients and turning today’s affordability constraints into tomorrow’s opportunity.